Traders of Environmental Progress

STX Group is a global environmental commodities trader offering physical and financial solutions across compliance and voluntary systems for energy, fuels, gas and carbon markets.

Traders of Environmental Progress

STX Group is a global environmental commodities trader offering physical and financial solutions across compliance and voluntary systems for energy, fuels, gas and carbon markets.

Emissions trading in safe hands

Vertis, a MiFID II trading firm, supports companies in navigating through carbon compliance schemes, including different EU Emissions Trading Systems, CBAM and CORSIA, in a cost-effective way

Blog

As the Netherlands accelerates its climate goals, many companies are asking: What exactly are DPRs, and how does the Dutch CO₂ levy impact my operations? In this post, we answer the most frequently asked questions about Dispensatierechten (DPRs), the Dutch CO₂ levy, and their interaction with the EU Emissions Trading System (EU ETS).

The Dutch CO₂ levy is a key instrument of the Dutch Climate Agreement, aiming to reduce CO₂ emissions by 49% by 2030 compared to 1990 levels. As of 2025, the levy is in effect. Although there were plans to abolish the tax or reduce the tariff to zero, authorities confirmed in this letter that a legal amendment is required, which will take effect no earlier than 2026.

However, for 2026, ETS1 covered industries and nitrous oxide plants (excluding incinerators will benefit from a CO2 levy reduction up to €78.67/tonne and an expansion of free allowances. As a result, no net revenue is expected in 2027; the planned recycling to the Klimaatfonds is scrapped and removed from the budget, according to this source.

A Dispensation Right (DPR) represents 1 tonne of CO₂e emissions. Companies subject to the levy must hold one DPR per each tonne emitted. Some DPRs are granted for free by the Dutch Emissions Authority (NEa) based on a company’s activity and efficiency.

Check your free DPR allocation here

Should a company have shortage or surplus of DPRS, they can also trade DPRs on the market to manage them.

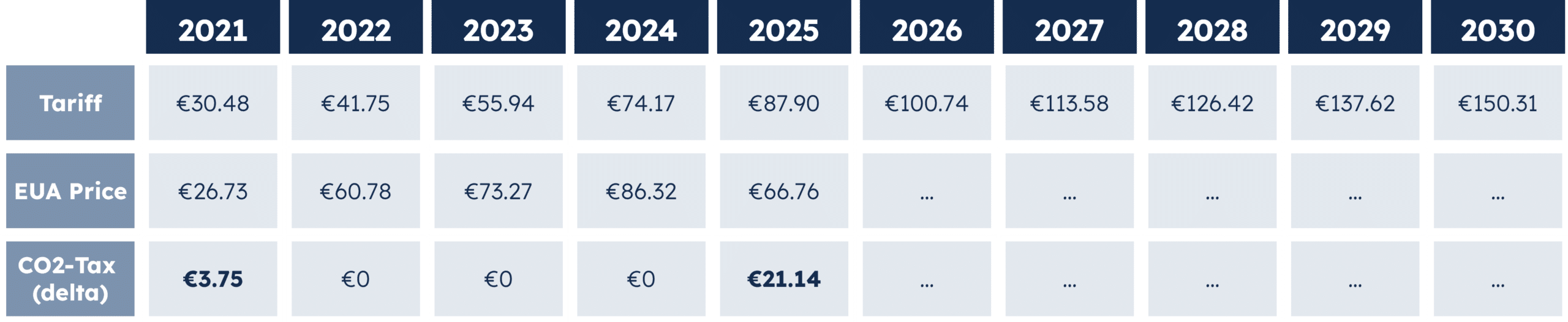

Through this CO₂ levy, the Netherlands introduced a minimum price for emissions on top of the ETS. Hence, if the Dutch CO2 tariff is higher than the EUA price, companies under the EU ETS must pay at least the specified Dutch CO2 tariff.

Should the Dutch CO2 tariff be lower than the EUA price*, ETS installations can deduct the total costs pay for the CO2 tax based from the EUA price paid, ensuring companies pay a minimum cost per tonne of CO₂.

*average EUA price in September–October

Non-ETS installations must cover their emissions with DPRs every year.

The DPR market price is determined by supply and demand, and certificates are only tradeable in the OTC market. Without the intervention of an exchange, market participants will likely need the support of intermediaries to connect their surplus or shortage with those of the market.

With over 27 years of experience in the compliance carbon market and an extensive network of collaborators, Vertis is your trusted partner in securing a timely and cost-effective compliance under the Dutch CO2 tax.

All companies must declare DPRs annually, keep an eye on the deadlines for each task below:

Receiving DPRs: May Y+1

DPRs are available in accounts from May. For instance, free allocation of DPRs corresponding to 2025 should be available to market participants by May 2026. However, market prices can be locked in today.

Transfer period: May–August T+1

The period to sell your surplus or acquire your shortages goes from May to August. For instance, for 2025 the transfer period goes from May-August 20206

Compliance deadline: September of year T+1.

For the 2025 compliance period, DPRs must be surrendered to the authorities by September 2026

Pay attention, Banking DPRs is not allowed. A surplus can only be traded in the same year and not be stored for future years. However, if you have paid the CO2-tax in the past and you currently have a surplus this may be used to cover up for the 5 previous years and ask a tax refund for these years.

Every year, the ICAP Emissions Trading Worldwide Status Report lands as one of the most anticipated publications in the carbon markets space. It’s the kind of docume.....